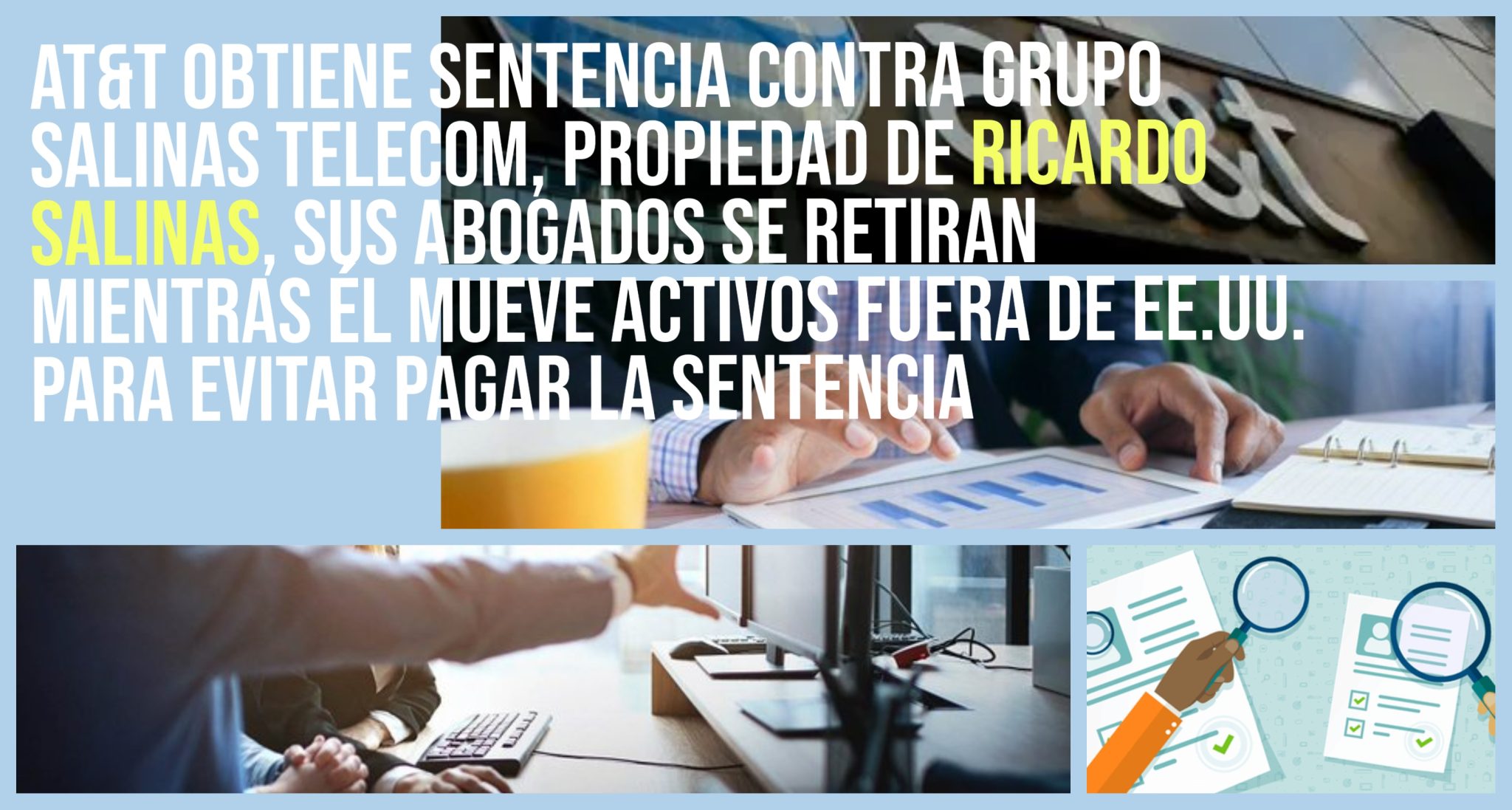

VANCOUVER, Canadá, 30-Sep-2024 — /EuropaWire/ — Astor Asset Management 3 Ltd informa que Ricardo Benjamín Salinas Pliego, presidente de Grupo Elektra, S.A.B. de C.V., enfrenta nuevas acusaciones por transferir activos fuera de Estados Unidos para evadir el pago de una sentencia de 20 millones de dólares derivada de una disputa contractual con AT&T.

La sentencia fue emitida el 29 de noviembre de 2023 por un tribunal estadounidense contra Grupo Salinas Telecom, S.A. de C.V. y Grupo Salinas Telecom II, S.A. de C.V., empresas vinculadas a Salinas Pliego. Documentos judiciales revelan que Grupo Salinas Telecom realizó transferencias rápidas de activos fuera de Estados Unidos solo tres días después de la sentencia.

Según los informes, 10,25 millones de dólares en acciones de Grupo Elektra fueron transferidos desde una correduría en EE.UU. a Banco Azteca en México. Además, se enviaron 5,65 millones de dólares a una entidad canadiense, Security International Investments, Inc., que supuestamente está vinculada a Salinas Pliego. También se han documentado otras transferencias y liquidaciones de activos que superan los 10 millones de dólares.

Por “razones estratégicas”, Salinas Pliego decidió no contar con representación legal en este caso, lo que ha sido interpretado como un intento de evitar el pago de la sentencia judicial. Esta acción, junto con el historial de las empresas de Salinas Pliego de alegar dificultades financieras para no pagar a sus acreedores, plantea serias preocupaciones sobre la transparencia y gobernanza en Grupo Elektra.

Salinas Pliego tiene un historial extenso de conductas financieras controvertidas, que incluyen acusaciones de fraude de valores, disputas por impuestos no pagados y deudas con acreedores. Sus recientes movimientos, incluidos los rápidos traslados de activos fuera de la jurisdicción estadounidense, han atraído un mayor escrutinio por parte de reguladores financieros y acreedores.

Astor Asset Management 3 Ltd también está involucrada en litigios con Salinas Pliego en el Reino Unido por el incumplimiento de un préstamo de 110 millones de dólares.

A medida que los mercados exigen cada vez más transparencia y responsabilidad, la gestión de estos asuntos legales y financieros por parte de Salinas Pliego será vigilada de cerca por inversores y reguladores.

SOURCE: EuropaWire